Payment for order flow explained simply: PFOF is compensation a broker receives for routing customer trades to a market maker, exchange, or other execution venue. It is one reason some brokers can offer commission-free trading, but it also creates a conflict because the venue paying the broker is not automatically the venue that gives the customer the best execution.

That does not mean every PFOF trade is bad. Some orders receive price improvement. Some brokers disclose routing practices clearly and measure execution quality seriously. The useful question is not only “Does this broker use PFOF?” It is “What execution quality did customers actually receive after spreads, speed, fill quality, and price improvement?”

This article is educational only. It is not personalized financial advice. For broader limitations, see Jivaro’s financial disclaimer.

Quick answer: what PFOF means for investors

A customer places a trade, the broker routes it, a market maker or venue executes it, and the broker may receive compensation for sending the order there. In the U.S., this is legal when brokers meet best-execution duties and disclosure rules. In the United Kingdom it is effectively prohibited for ordinary retail and professional client order flow under FCA rules, and the European Union has adopted an explicit prohibition with limited transitional relief through June 30, 2026.

In practical terms, PFOF turns the “free trading” question into an execution-quality question. A $0 commission is visible. The spread, fill quality, routing incentive, and missed price improvement are less visible.

Payment for order flow explained in plain English

When a customer places an order, the broker usually has choices. A broker may route a stock order to an exchange, another exchange, an electronic communications network, a market maker, or even fill the order through internalization. A market maker is a firm that stands ready to buy or sell at quoted prices, and some market makers pay brokers for routing orders to them. That payment is called payment for order flow.

The core economics are straightforward. Retail order flow can be attractive to wholesalers because it is often less informed than institutional flow. A market maker may be willing to execute the order at a slightly better price than the public quote, earn part of the spread, and pay the broker for the order flow.

The conflict is also straightforward. If a broker receives compensation from a venue, the broker has an economic reason to route orders there. U.S. rules do not ban that by default, but the broker still has to seek best execution. That is why PFOF should be judged by execution quality, not only by whether the broker charges a visible commission.

How PFOF works

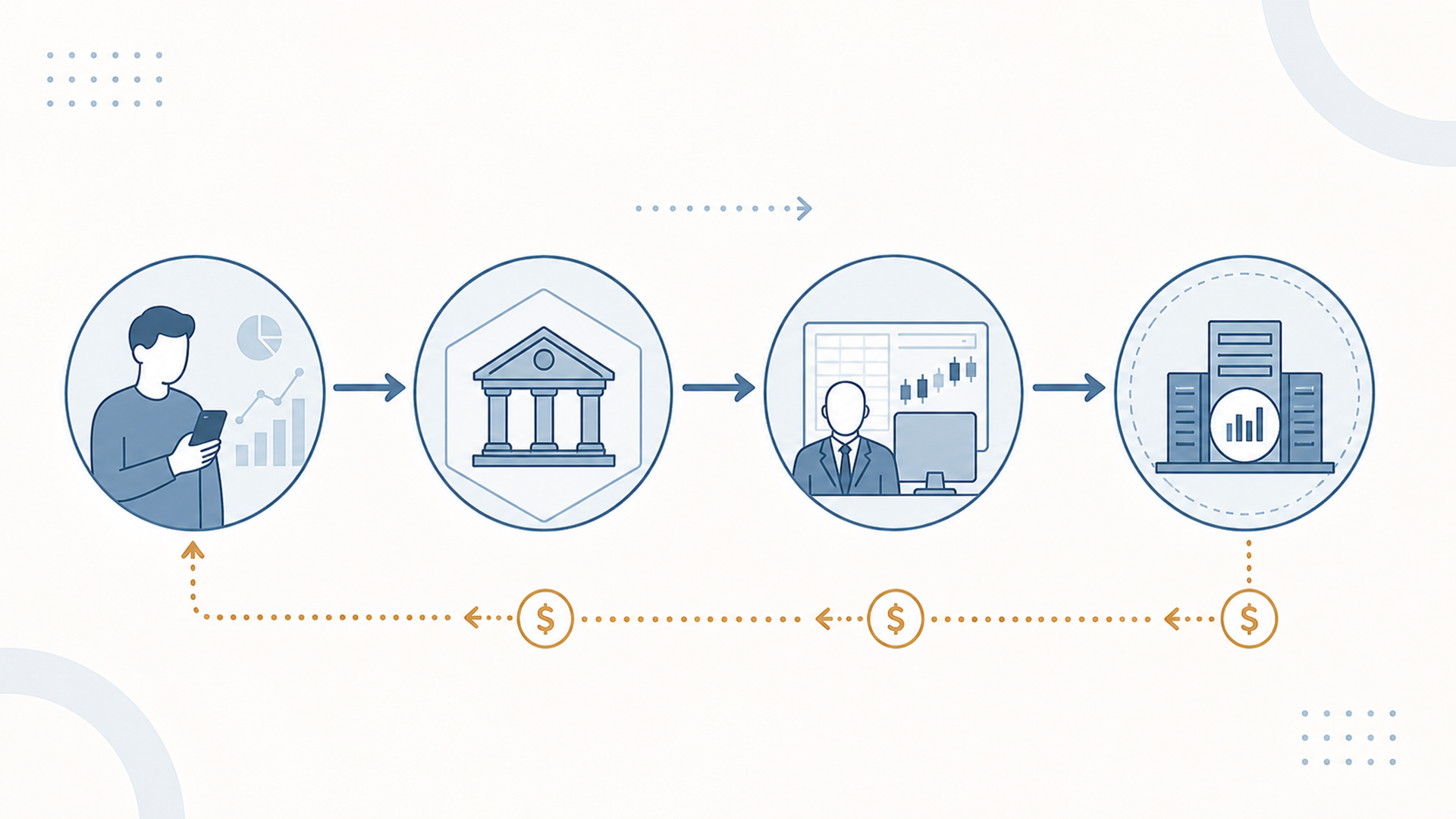

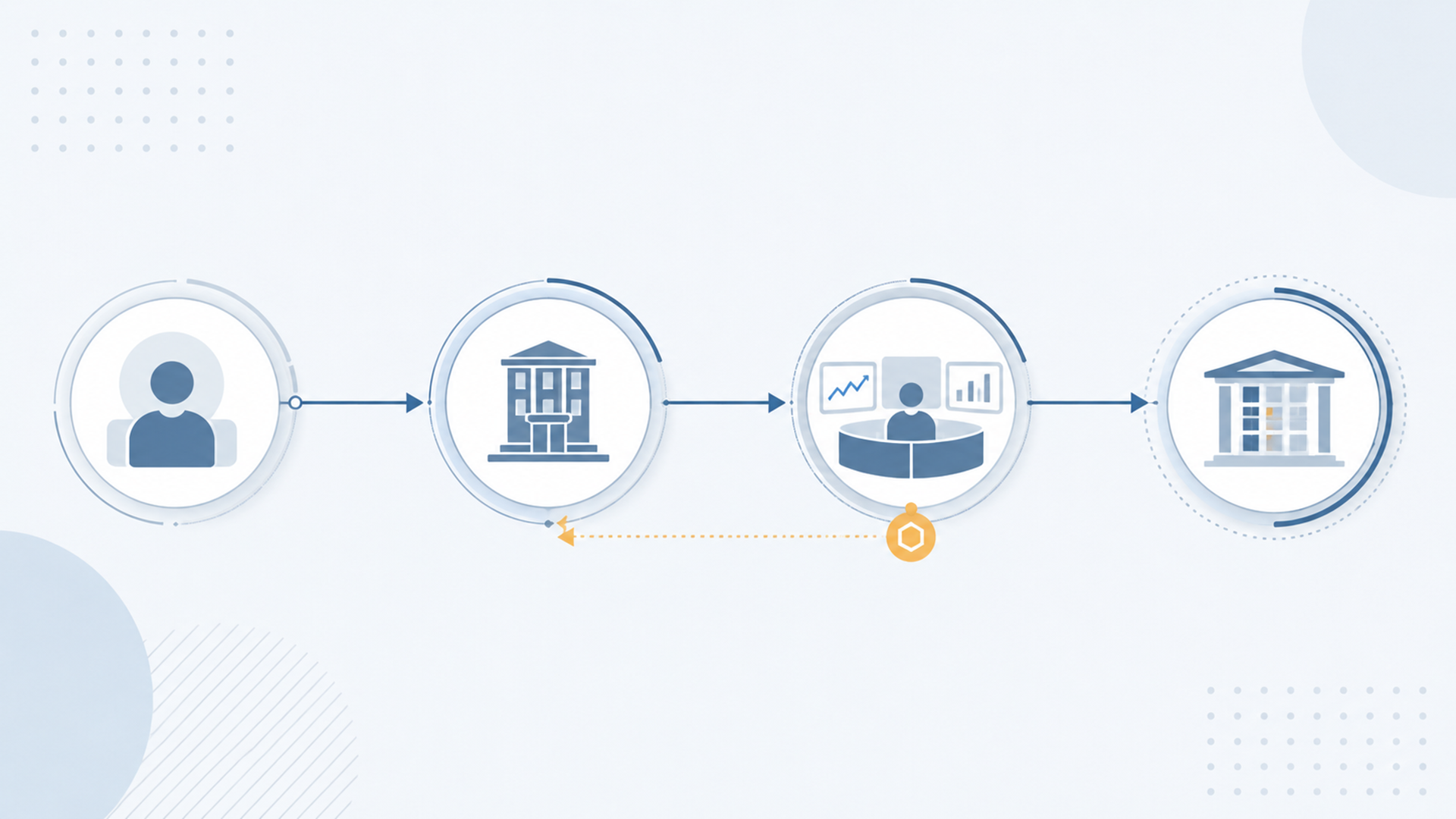

A typical PFOF order-routing chain has four parts.

A retail investor places a market or limit order through a brokerage app or website.

The broker decides where to send the order based on its routing policy and best-execution process.

A market maker, exchange, or other venue executes the order, sometimes with price improvement.

The broker may receive PFOF, rebates, discounts, or other compensation tied to routed order flow.

The customer may see the trade as “commission-free,” but the economics still exist. The market maker can earn money from the bid-ask spread or other execution economics. The broker may earn routing compensation. The customer’s real cost depends on the execution price, the spread, the speed and likelihood of execution, and whether the order received meaningful price improvement.

Platform examples: Robinhood, Fidelity, and Schwab

Broker examples are useful because PFOF is not one uniform model. The same word can cover different asset classes, different payment formulas, and different disclosure styles. These examples are not recommendations; they show how readers can compare routing models.

| Platform example | What it illustrates | What to check |

|---|---|---|

| Robinhood | Robinhood’s annual disclosure states that Robinhood Financial routes customer equity and options orders to Robinhood Securities, which routes orders to market centers and receives payment for order flow from those market centers. | Read its annual customer disclosure and current Rule 606 reports to separate equities, options, and routing formulas. |

| Fidelity | Fidelity is useful as a contrast because its public execution-quality page emphasizes price improvement, Rule 605 data, Rule 606 reports, and order-flow management rather than making PFOF the headline model. | Use Fidelity’s execution-quality page and current Rule 606 reports to verify routing details by asset class. |

| Charles Schwab | Schwab says it receives rebates from liquidity providers and exchanges as part of common industry practice, but also says best execution takes priority and eligible rebates are not a routing consideration. | Read Schwab’s order-routing disclosure, retail execution-quality statistics, and current Rule 606 reports. |

The platform lesson is simple: a broker’s PFOF status is not enough. The better review looks at order type, asset class, execution price, price improvement, spread, speed, fill quality, and whether routing incentives are clearly disclosed.

PFOF pros and cons

- Can help support commission-free trading for retail investors.

- Market makers may provide price improvement versus the displayed quote.

- Retail orders can sometimes be executed quickly by large liquidity providers.

- Disclosure rules give investors a way to inspect routing relationships through Rule 606 reports.

- Creates a conflict between broker revenue and customer execution quality.

- Can make the true cost of “free” trading harder to see.

- May differ sharply across stocks, ETFs, options, and crypto-related products.

- Requires investors to read disclosures that are often technical and hard to compare.

The balanced view is that PFOF is neither automatically harmless nor automatically abusive. It is a structure that needs evidence. The evidence should come from current routing reports, execution-quality statistics, and regulatory disclosures—not from slogans about free trades.

The main conflict: lower visible costs vs execution quality

The PFOF debate exists because two things can be true at the same time. First, zero-commission trading can lower a visible cost for investors. Second, routing compensation can create a conflict that affects how orders are handled.

FINRA has warned that member firms may not let payment for order flow interfere with best execution. Best execution requires reasonable diligence to seek the most favorable terms reasonably available under the circumstances, and price is a key concern for most retail customers. FINRA has also made clear that disclosure does not erase the legal duty to provide best execution. See FINRA Regulatory Notice 21-23.

That is why “the trade was free” is an incomplete answer. The correct comparison is not $0 commission versus a visible commission in isolation. It is the all-in experience: execution price, spread, speed, fill probability, routing incentive, and whether better execution was reasonably available elsewhere.

What U.S. rules require

In the U.S., PFOF is allowed, but it sits inside a disclosure and best-execution framework.

| Rule or duty | What it does | Why it matters for PFOF |

|---|---|---|

| Best execution | Brokers must use reasonable diligence to seek favorable execution terms under prevailing market conditions. | PFOF cannot be allowed to drive routing decisions at the expense of customer execution quality. |

| SEC Rule 607 | Brokers must disclose policies on receiving payment for order flow when opening a new account and annually afterward. | Customers should be told whether the broker receives PFOF and how routing policies work. See 17 CFR 242.607. |

| SEC Rule 606 | Brokers must publish quarterly reports on routing of non-directed orders, including venue relationships and payment information. | These reports show where orders are routed and what payment, rebates, fees, or arrangements may influence routing. See 17 CFR 242.606. |

| SEC Rule 605 updates | The SEC adopted amendments in 2024 to improve public execution-quality reporting, including broader reporting scope and more granular execution-quality information. | Better execution-quality data can make broker comparisons more meaningful. See the SEC’s Disclosure of Order Execution Information final rule. |

The disclosure stack is helpful, but it is still not simple. A reader comparing brokers should expect to look at more than one document: annual disclosures, Rule 606 routing reports, execution-quality pages, and the broker’s explanation of routing priorities.

Where PFOF is banned or effectively prohibited

PFOF is treated differently outside the U.S. In the United Kingdom, the FCA’s position is that PFOF creates a clear conflict of interest and is generally unlikely to be compatible with inducement rules while also risking best-execution compliance. The FCA defined PFOF as a broker receiving payment from market makers in exchange for sending order flow to them. See the FCA’s finalised guidance on PFOF.

The European Union has moved to an explicit prohibition. Regulation (EU) 2024/791 inserted Article 39a, titled “Prohibition of receiving payment for order flow.” It prevents investment firms acting for retail clients and certain professional clients from receiving a fee, commission, or non-monetary benefit from a third party for executing or forwarding orders to a particular execution venue. Some member states can use a transitional exemption until June 30, 2026. See Regulation (EU) 2024/791.

For global readers, the takeaway is that PFOF is mainly a U.S. market-structure issue. It is not a universally accepted brokerage practice.

What research says about PFOF

Research does not support a lazy conclusion that PFOF is always good or always bad. The evidence is more uncomfortable: execution quality can vary by broker, asset class, and market structure.

A large study by Christopher Schwarz, Brad Barber, Xing Huang, Philippe Jorion, and Terrance Odean generated 85,000 simultaneous market orders across brokerage accounts and found that execution prices varied significantly across brokers. The authors also found that variation in PFOF did not explain all of the execution-quality differences. See The “Actual Retail Price” of Equity Trades.

A randomized controlled trial by Bradford Levy found meaningful heterogeneity among PFOF-based brokers. In that study, some PFOF-based brokers provided little price improvement while others provided statistically significant price improvement. See Price Improvement and Payment for Order Flow.

Options deserve separate attention. A Review of Financial Studies paper finds that PFOF is more prevalent in options than in stocks, with more than half of options trading involving orders purchased by wholesalers. The same paper finds that options auctions save investors over $47 million daily through price improvement, while also showing that wholesalers need revenue sources to pay for the order flow. See the Review of Financial Studies article.

Crypto-related PFOF can look even more opaque. A 2025 SEC DERA working paper on Robinhood Crypto token introductions found that, compared with equity and options PFOF, crypto PFOF lacked transparency and generated significantly higher fees in the sample studied. See the SEC DERA working paper, How Does Payment for Order Flow Influence Markets?

How to evaluate a broker’s PFOF model

A reader does not need to become a market-structure specialist to ask better questions. The practical checklist is short.

| Question | Why it matters | Where to look |

|---|---|---|

| Does the broker receive PFOF? | This identifies the routing conflict, but not the full execution outcome. | Annual customer disclosure, Rule 607 disclosure, broker order-routing page. |

| How are stocks, ETFs, and options treated differently? | Options PFOF can be structurally different and often more economically significant than stock PFOF. | Rule 606 reports split by NMS stocks and listed options. |

| What execution quality does the broker show? | Price improvement, effective spread, execution speed, and fill quality matter more than marketing claims. | Rule 605 data, execution-quality pages, broker reports. |

| Are routing incentives clearly disclosed? | Payment schedules, rebates, volume tiers, and venue relationships can shape incentives. | Rule 606 quarterly reports and order-routing disclosures. |

| Can the broker explain why the venue was chosen? | Best execution should come from a process, not just a payment relationship. | Order-routing policy, best-execution disclosures, customer-specific routing reports when available. |

For a broader review process, use Jivaro’s broker comparison methodology. The better broker review does not rank platforms on commission alone. It weighs execution quality, product scope, risk disclosures, costs, account protections, platform design, and the way the broker makes money.

FAQ

Is payment for order flow legal?

In the U.S., yes, provided brokers satisfy best-execution duties and disclosure requirements. In the U.K., PFOF is effectively prohibited for ordinary retail and professional client order flow under FCA guidance. In the EU, Regulation (EU) 2024/791 adopted an explicit prohibition with limited transitional relief for certain member states through June 30, 2026.

Does PFOF mean the investor gets a worse price?

Not always. Some orders receive price improvement, and some market structures can generate meaningful price improvement. But PFOF creates a conflict, and research shows execution quality can vary materially across brokers. That is why the broker’s actual execution data matters.

Is PFOF only about stocks?

No. PFOF also matters in options, and the economics can be larger there because options markets have wider spreads and different auction mechanics. Crypto-related order-flow models can have still different transparency and fee issues.

How can someone check whether a broker receives PFOF?

Start with the broker’s order-routing disclosure and Rule 607 disclosure. Then review the broker’s quarterly Rule 606 reports, which show routing venues and payment, rebate, fee, and relationship details for non-directed order flow.

Does commission-free trading mean trading is actually free?

No. A trade can have no visible commission and still have economic costs through spreads, execution quality, price movement, options contract fees, margin costs, or product-specific charges. PFOF is one reason headline pricing should not be the only comparison point.

Conclusion

PFOF is best understood as a tradeoff built into modern brokerage economics. It can help support low-commission or commission-free trading, and some orders may receive price improvement. But it also creates a conflict that has to be controlled through best execution, disclosure, routing oversight, and measurable execution quality.

The strongest conclusion is not “PFOF is always bad” or “PFOF is always fine.” The stronger conclusion is that brokerage platforms should be judged by the full order-routing result. Readers should look past the headline commission and ask what happened to the order after they clicked buy or sell.

For more context on finance and investing topics, see the Jivaro finance hub. For a shorter companion overview, use Jivaro’s PFOF article.

References

- Investor.gov: Executing an Order

- FINRA Regulatory Notice 21-23: Best Execution and Payment for Order Flow

- 17 CFR 242.606: Disclosure of Order Routing Information

- 17 CFR 242.607: Customer Account Statements

- SEC Final Rule: Disclosure of Order Execution Information

- Robinhood Annual Customer Disclosure Notice

- Fidelity: Commitment to Execution Quality

- Charles Schwab: Order Routing

- FCA: Guidance on the Practice of Payment for Order Flow

- Regulation (EU) 2024/791

- Schwarz, Barber, Huang, Jorion, and Odean: The “Actual Retail Price” of Equity Trades

- Levy: Price Improvement and Payment for Order Flow

- Review of Financial Studies: Options, Auctions, and Payment for Order Flow

- SEC DERA Working Paper: How Does Payment for Order Flow Influence Markets?